Loans: Understanding the math behind flat vs amortized rate

Disclaimer: This is not financial advice. Treat the information here as tools to understand what you are in for when taking a loan

(Just want the tools to calculate your loan? Skip to the bottom of this article)

Loans are inevitable for the large purchases in life. Not helping are the many confusing terms to describe the most common loans. Home loans go by “mortgages” and “amortized” loans. Personal and hire-purchase loans are called “flat rate” loans. What does it all mean?

The picture becomes simpler after looking at how interest is charged. In doing so, all loans boil down to two types:

- Interest calculated on entire principal over loan duration

Common names: Flat rate - Interest calculated on remaining principal after each given period

Common names: Amortized, mortgage, monthly, reducing rate, fixed rate (interest fixed upfront), floating rate (interest varies by base lending rate)

For simplicity, let’s call them flat rate and amortized loans. (P.S. Let me know if you come across other names for these loans in the comments =))

With that out of the way, let’s figure out how how to calculate two important things about any loan:

- The monthly repayment

- How much interest to pay

Flat rate loans

Monthly repayment is calculated at start of a flat rate loan based on three things:

- Principal aka loan amount, P

- Yearly interest rate, i

- Years to repay, y

The equation to calculate monthly repayment is:

Monthly repayment = (P+(Piy))/(12y)

Where:

Piycalculates the interest charged for each year of the loanP+(Piy)gives the total sum to pay over the entire loan(12y)converts the years to repay into months

To get the interest paid, a fast calculation is to subtract the total paid over the years with the principal

Interest paid = (Monthly repayment * 12y) — P

Calculations for flat rate loan

Take the following loan as an example:

- Principal aka amount to borrow, P = $100,000

- Yearly interest rate, i = 5%

- Years to repay, t = 5 years

Thus, the monthly repayment is:

Monthly repayment = (100000+(100000*0.05*5))/(12*5) = $2083.33

and the interest paid is:

Interest paid = (2083.33 * 12*5) — 100000 = $25000

Amortized loans

Amortized loans typically charge each month. Thus, interest is calculated at the end of each month based on the remaining principle. To perform this calculation, one would need:

- Principal aka amount to borrow, P

- Monthly interest rate, r. This is the annual interest rate divided by 12.

- Months to repay, n

The equation to calculate monthly repayment is commonly depicted as (ref):

Monthly repayment = Pr(1+r)^n/((1+r)^n — 1)

Simplifying by dividing the top and bottom of the fraction with (1+r)^n:

Monthly repayment = Pr / (1 — (1+r)^-n)

Reading it now:

Pris the interest to pay for this month(1 — (1+r)^-n)represents the repayment rate divider. A shorter repayment term,nreduces this divider. This increases the monthly repayment amount since there is less time to pay the loan back.

Calculations for amortized loan

Let’s calculate for an amortized loan to be paid back in 1 year:

- Principal aka loan amount, P = $100,000

- Yearly interest rate, i = 5%. Thus, r = 0.05/12 = 0.004167

- Years to repay, t = 1 year. Thus, n = 1*12 = 12 months

The equation returns:

Monthly repayment = 100000*0.004167 / (1 — (1+0.004167)^-12) = $8560.75

As for the total interest paid, lets again subtract the total paid over the months with the principal:

Interest paid = (8560.75 * 12*1) — 100000 = $2729

Proof for calculated monthly repayment rate of amortized loan

The idea here is to manually apply the same monthly interest rate each month on the remaining principal. Here’s a table showing how the principal declines to zero by the 12th month with each monthly repayment of $8560.75. Note the slight inaccuracy inherent to the monthly repayment equation shown at the 13th month:

| Month | Remaining principal | Interest to pay | Repayment | Reduction in principal |

|-------|---------------------|-----------------|-----------|------------------------|

| 1 | 100000 | 416.67 | 8560.75 | 8144.08 |

| 2 | 91855.91667 | 382.73 | 8560.75 | 8178.02 |

| 3 | 83677.89965 | 348.66 | 8560.75 | 8212.09 |

| 4 | 75465.80757 | 314.44 | 8560.75 | 8246.31 |

| 5 | 67219.49843 | 280.08 | 8560.75 | 8280.67 |

| 6 | 58938.82968 | 245.58 | 8560.75 | 8315.17 |

| 7 | 50623.65813 | 210.93 | 8560.75 | 8349.82 |

| 8 | 42273.84004 | 176.14 | 8560.75 | 8384.61 |

| 9 | 33889.23104 | 141.21 | 8560.75 | 8419.54 |

| 10 | 25469.68617 | 106.12 | 8560.75 | 8454.63 |

| 11 | 17015.05986 | 70.90 | 8560.75 | 8489.85 |

| 12 | 8525.205947 | 35.52 | 8560.75 | 8525.23 |

| 13 | -0.02 | | | |Where:

Interest to pay = Remaining principal * monthly interest rate

Reduction in principal = Repayment — Interest to pay

Subsequent remaining principal = Previous remaining principal — Reduction in principal

Ok, we now know the math. Why does it matter?

As a consumer, the two main concerns when taking any loan are:

- To pay the least interest possible. All interest is another charge on top of the loan principal.

- To pay off the loan as soon as possible. A longer-term loan charges more interest. Plus, it ties up your cash.

This gets confusing when a bank offers the same loan as flat rate and amortized. Let’s say a bank offers the following interest rates for a 10 year loan:

- Flat rate: 3.95% per year

- Amortized: 5.77% per year

At first glance, the amortized loan appears to charge more interest. However, after calculating the monthly repayment on a $100,000 loan:

- Flat rate:

(100000 + (100000*0.0395*10))/(12*10) = 1163

Interest paid:1163*(12*10) — 100000 = 39560 - Amortized:

100000*(0.0577/12)/(1- ((1+(0.0577/12))^-(10*12))) = 1099

Interest paid:1099*(12*10) — 100000 = 31880

Now what if both loans have the same rate, say 5%:

- Flat rate:

(100000 + (100000*0.05*10))/(12*10) = 1250

Interest paid:1250*(12*10) — 100000 = 50000 - Amortized:

100000*(0.05/12)/(1- ((1+(0.05/12))^-(10*12))) = 1061

Interest paid:1061*(12*10) — 100000 = 27320

Thus, the more expensive loan in both situations is the flat rate loan.

All right, how can I do this math?

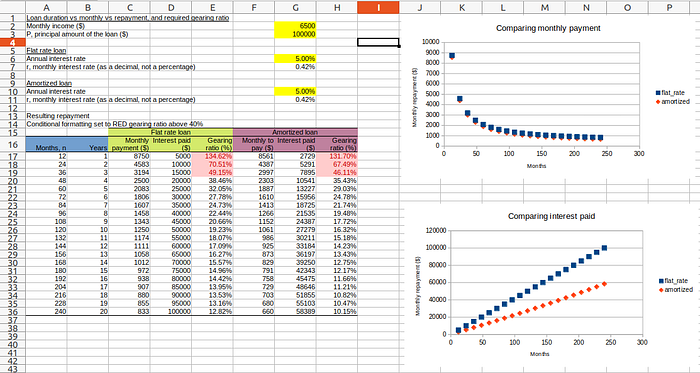

Here’s a spreadsheet. Feel free to download it using Right Click > Save Link As:

Now a peek at what it can do. The fields in YELLOW take your input:

Play with it to see how the loan repayment changes for a given principal by changing:

- Annual/Yearly interest rate, i

- Loan duration in months, n

I also included a gearing ratio. This is what percent of your monthly income goes to the loan. The common advice I receive is to keep it below 40%.

Don’t want do the math yourself? Here’s a bunch of online calculators

- Flat rate: emi-calc.com,

- Amortized: CalculatorSoup, Calculators.org, NerdWallet

- Flat rate and amortized: Marketfeed.com

I hope you are now better armed before meeting your banker! Let me know if the comments if you follow any advice about getting a loan.

References

Furey, Edward “Loan Calculator” at https://www.calculatorsoup.com/calculators/financial/loan-calculator.php from CalculatorSoup, https://www.calculatorsoup.com — Online Calculators

On amortized, interest-only, and credit card loans: https://www.thebalancemoney.com/loan-payment-calculations-315564

About flat rate loans vs amortized: https://www.directlending.com.my/blog/flat-effective-fixed-floating-interest-rate-loans/